All Categories

Featured

Table of Contents

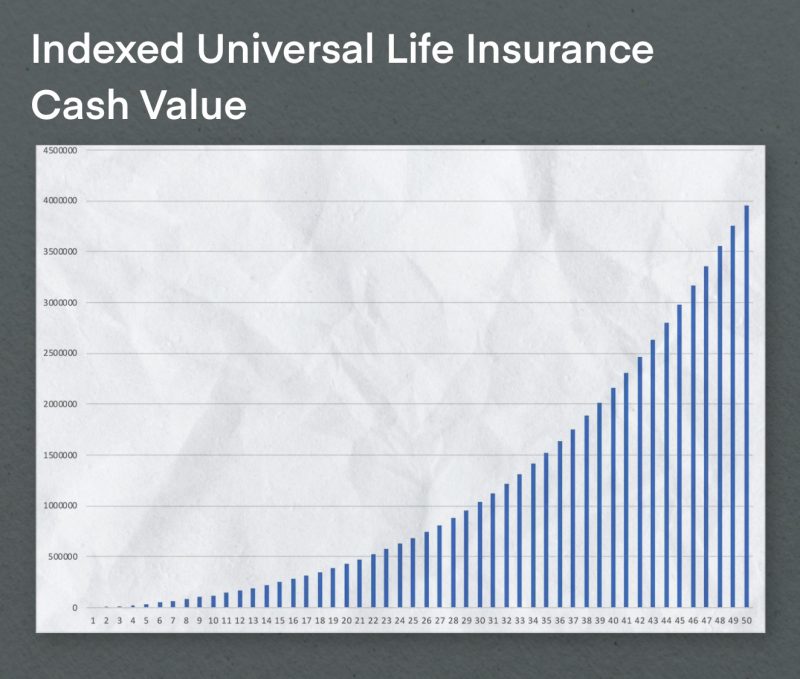

Below is a hypothetical contrast of historical performance of 401(K)/ S&P 500 and IUL. Allow's assume Mr. SP and Mr. IUL both had $100,000 to conserved at the end of 1997. Mr. SP invested his 401(K) money in S&P 500 index funds, while Mr. IUL's money was the money worth in his IUL plan.

IUL's policy is 0 and the cap is 12%. After 15 years, at the end of the 2012, Mr. SP's profile expanded to. Because Mr. IUL never lost cash in the bear market, he would have two times as much in his account Also much better for Mr. IUL. Considering that his money was conserved in a life insurance policy policy, he does not need to pay tax! Naturally, life insurance shields the family and supplies sanctuary, foods, tuition and clinical costs when the insured passes away or is seriously ill.

Iul K

The plenty of choices can be mind boggling while researching your retired life investing options. There are particular choices that ought to not be either/or. Life insurance policy pays a survivor benefit to your recipients if you should pass away while the policy is in result. If your household would encounter monetary hardship in the event of your death, life insurance policy uses satisfaction.

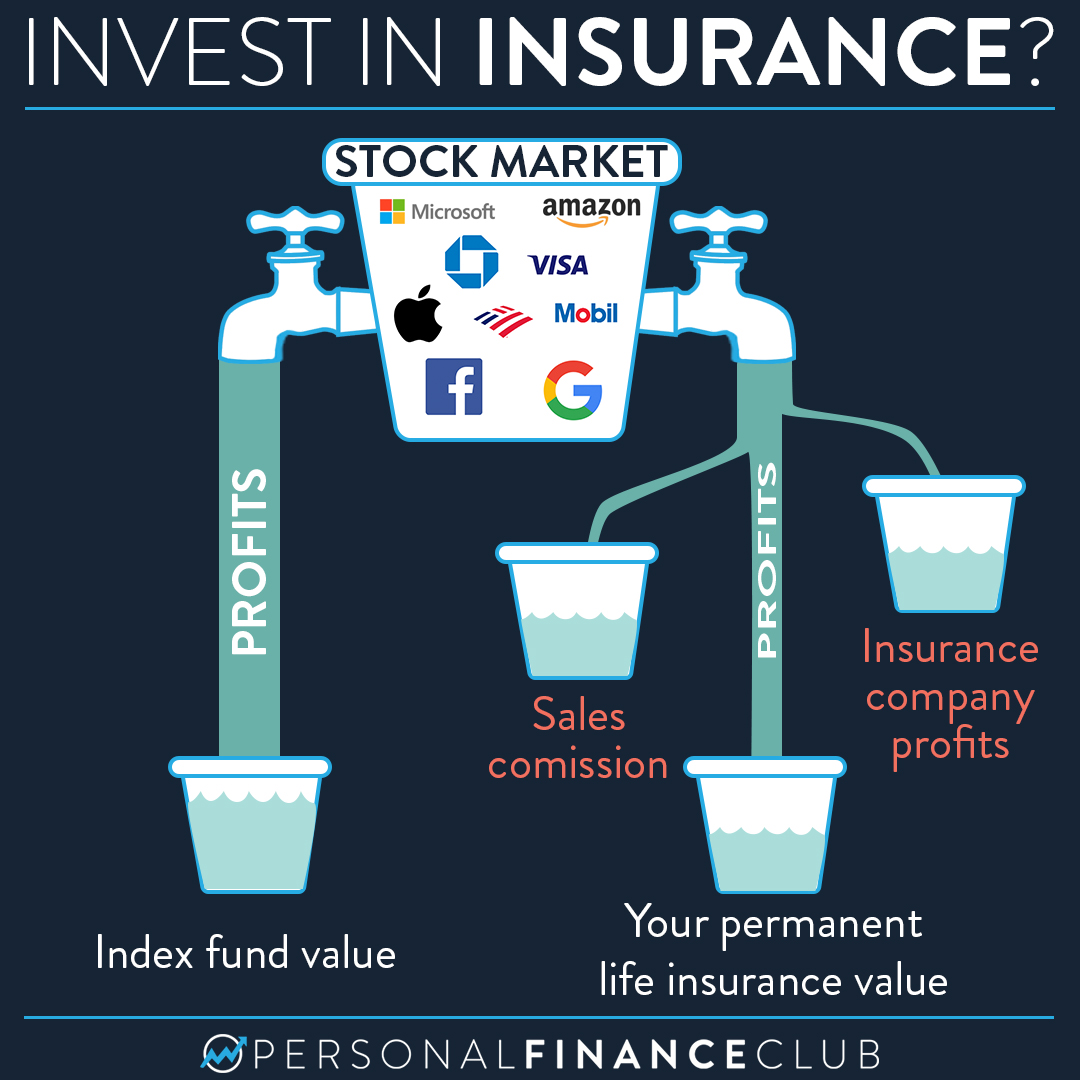

IUL policies is a perfect fit for the infinite banking strategy. instant IUL insurance quotes from brokers. Infinite banking with Indexed Universal Life lets you take control of your finances

By borrowing against your Indexed Universal Life policy’s cash value, you can fund major expenses while your money continues to grow tax-free. Knowledgeable agents help you structure policies for infinite banking.

With features like cash value growth and tax-free loans, IUL supports personal and business goals. Learn how IUL can transform your finances with a free consultation from a licensed broker.

It's not one of one of the most rewarding life insurance policy financial investment plans, however it is one of one of the most safe. A form of irreversible life insurance coverage, universal life insurance policy allows you to select exactly how much of your premium goes towards your survivor benefit and just how much enters into the plan to accumulate money worth.

:max_bytes(150000):strip_icc()/indexed-universal-life-insurance.asp-Final-9f72d52f11d643c693ab8b3600f3cd27.png)

In addition, IULs permit insurance holders to obtain car loans versus their policy's cash worth without being tired as income, though overdue balances may go through tax obligations and fines. The primary benefit of an IUL plan is its potential for tax-deferred growth. This implies that any profits within the plan are not taxed until they are taken out.

Conversely, an IUL plan might not be one of the most ideal cost savings strategy for some people, and a conventional 401(k) could verify to be much more helpful. Indexed Universal Life Insurance Policy (IUL) policies use tax-deferred growth potential, defense from market slumps, and fatality advantages for recipients. They allow policyholders to make interest based upon the performance of a stock exchange index while securing against losses.

Is Iul Good For Retirement

Companies might likewise provide matching contributions, even more enhancing your retired life savings potential. With a conventional 401(k), you can reduce your taxed earnings for the year by adding pre-tax dollars from your income, while additionally profiting from tax-deferred development and company matching contributions.

Numerous companies also give coordinating contributions, efficiently offering you totally free cash in the direction of your retirement. Roth 401(k)s function in a similar way to their traditional equivalents but with one secret difference: tax obligations on payments are paid upfront rather than upon withdrawal throughout retirement years (iul life insurance uk). This means that if you expect to be in a greater tax obligation bracket during retired life, adding to a Roth account might conserve on taxes in time compared with investing entirely via conventional accounts (source)

With lower administration costs typically contrasted to IULs, these kinds of accounts permit capitalists to save money over the long term while still profiting from tax-deferred growth possibility. Furthermore, lots of popular low-cost index funds are offered within these account types. Taking distributions before getting to age 59 from either an IUL plan's cash worth via financings or withdrawals from a typical 401(k) plan can lead to negative tax obligation implications otherwise handled very carefully: While borrowing against your plan's cash value is generally thought about tax-free up to the amount paid in premiums, any overdue funding balance at the time of fatality or policy abandonment may go through revenue taxes and fines.

Iul Vs Roth Ira

A 401(k) gives pre-tax financial investments, company matching payments, and potentially more financial investment options. The disadvantages of an IUL include higher management costs compared to traditional retirement accounts, restrictions in investment choices due to plan restrictions, and possible caps on returns throughout strong market performances.

While IUL insurance policy may prove beneficial to some, it is very important to recognize just how it functions prior to purchasing a policy. There are several pros and cons in comparison to other kinds of life insurance policy. Indexed universal life (IUL) insurance policy plans offer better upside potential, versatility, and tax-free gains. This kind of life insurance policy offers permanent coverage as long as costs are paid.

companies by market capitalization. As the index moves up or down, so does the price of return on the cash worth part of your plan. The insurance coverage firm that releases the plan may offer a minimum surefire price of return. There may likewise be a ceiling or rate cap on returns.

Economic professionals often recommend living insurance coverage that amounts 10 to 15 times your annual earnings. There are a number of disadvantages connected with IUL insurance coverage plans that movie critics fast to explain. For instance, someone that establishes the plan over a time when the marketplace is choking up can finish up with high premium payments that do not add in all to the cash money worth.

Aside from that, remember the complying with various other factors to consider: Insurance policy business can establish participation rates for just how much of the index return you get every year. Let's claim the plan has a 70% participation price. If the index grows by 10%, your cash money worth return would be just 7% (10% x 70%)

On top of that, returns on equity indexes are often covered at a maximum amount. A plan might say your optimum return is 10% per year, despite exactly how well the index executes. These limitations can limit the real price of return that's credited toward your account annually, despite just how well the plan's hidden index does.

How Does An Iul Compare To A 401(k)?

It's crucial to consider your individual danger tolerance and investment goals to guarantee that either one aligns with your total strategy. Whole life insurance policy policies usually include an ensured rate of interest price with foreseeable premium amounts throughout the life of the plan. IUL plans, on the other hand, offer returns based upon an index and have variable premiums over time.

There are several other sorts of life insurance policy plans, discussed listed below. offers a set benefit if the policyholder passes away within a set amount of time, typically between 10 and three decades. This is one of the most affordable kinds of life insurance policy, as well as the simplest, though there's no money worth accumulation.

Iul Vs 401k Retirement Benefits

The policy obtains worth according to a fixed schedule, and there are fewer charges than an IUL policy. They do not come with the flexibility of adjusting premiums. includes also more adaptability than IUL insurance policy, indicating that it is also a lot more complicated. A variable policy's cash money value might depend on the performance of certain supplies or various other protections, and your costs can likewise change.

%20Vs%20401(k)%3A%20How%20They%20Differ%20In%20Investment%20Options){kind=link}

Table of Contents

Latest Posts

Term Insurance Vs Universal Life

Signature Indexed Universal Life

Gul Policy

More

Latest Posts

Term Insurance Vs Universal Life

Signature Indexed Universal Life

Gul Policy